The Great Rotation Playbook — Theme 3: The Industrial Renaissance

The Manual of Ideas for Investing in the 3D World

This report builds on the foundational essay “The Great Rotation” and previously released parts of The Great Rotation Playbook — “The Energy Backbone” and “Critical Minerals & The Mining Supply Cliff.”

“Grassroots Macro,” as described by Bob Robotti, highlights a structural shift favoring the “boring” economy. The West, particularly North America, possesses a sustainable, multi-decade competitive advantage rooted in low-cost energy. This advantage is fueling a re-industrialization and “friend-shoring” boom, reversing decades of offshoring.

While the 2D world of software faces deflationary pressures from AI, the 3D world of industrial manufacturing and logistics is entering a renaissance. The beneficiaries are the companies that make the nuts, bolts, glass, and specialty materials that hold the physical world together. These businesses, often ignored by growth-obsessed investors, are now positioned to compound value through operational excellence, consolidation, and the return of industrial capacity to the West.

This report serves as a playbook for “Intelligent Investing 3D.” It moves beyond the macro thesis articulated in our foundational essay to identify actionable ideas within the Industrial sector, specifically targeting Chemicals, Steel, Diversified Industrials, Pulp & Paper, and Recycling. The analysis synthesizes insights from leading real-asset managers including Massif Capital, Horizon Kinetics, and Goehring & Rozencwajg, alongside data from major investment banking research divisions.

The core finding is that the “Old Economy” is not merely rebounding; it is undergoing a metamorphosis into a high-technology, capital-disciplined, and geostrategically critical ecosystem. The build-out of AI infrastructure is voraciously physical. It requires specific fluoropolymers for thermal management, grain-oriented electrical steel for voltage transformation, and sustainable fiber for packaging and fuel. Value is shifting from the digital economy to the industrial economy.

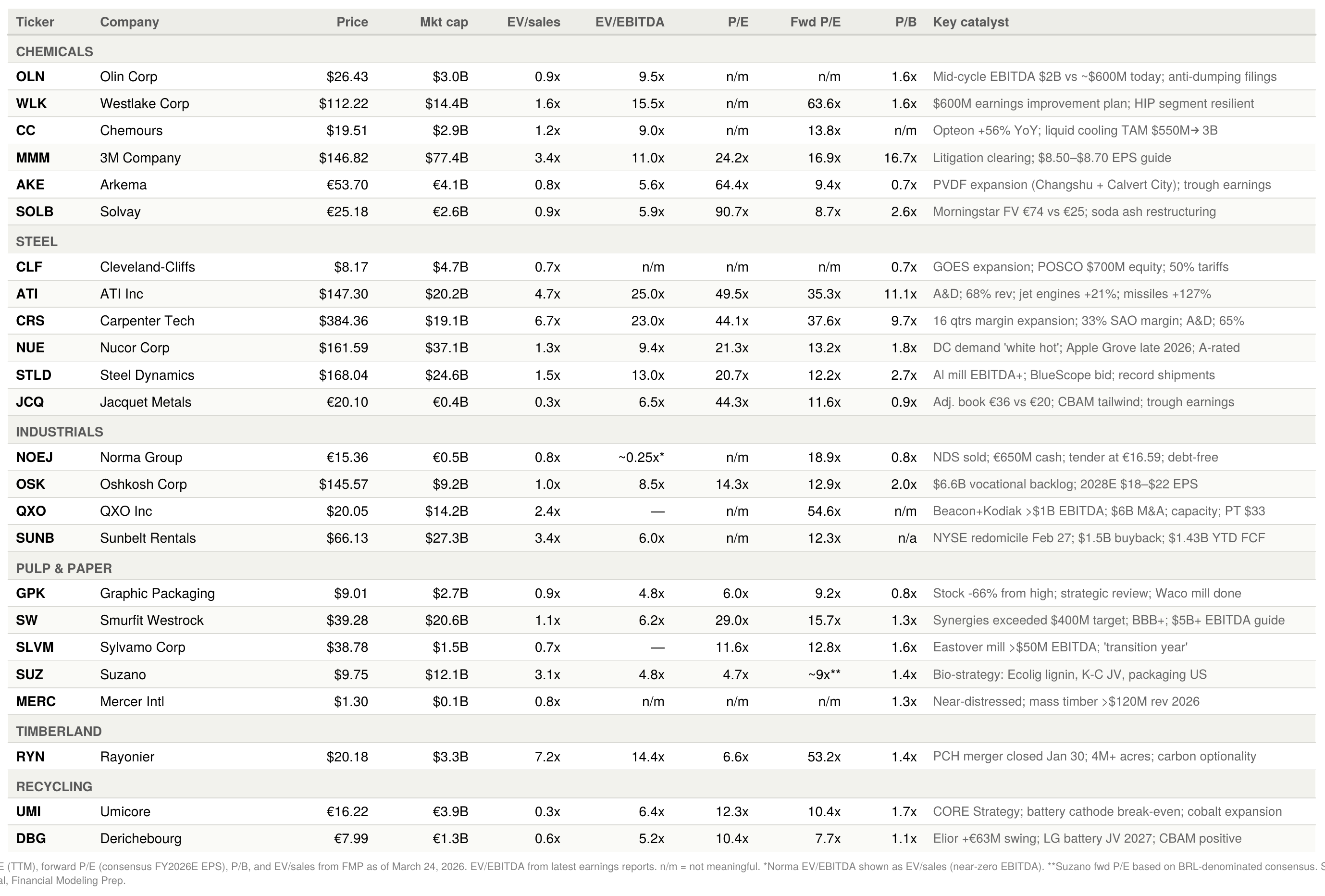

Companies mentioned inside:

Chemicals

The chemical industry stands at the intersection of energy policy and high-tech manufacturing. The investment thesis relies on two pillars: the geographic arbitrage of energy costs and the critical role of specialty chemicals in the AI hardware stack.

US Advantage vs. European Deindustrialization

A profound divergence has emerged between the North American and European chemical sectors. The US chemical industry benefits from a structural feedstock advantage: abundant, low-cost natural gas and ethane derived from the shale revolution. Conversely, the European sector faces an existential crisis driven by high energy costs and regulatory burdens.

Chemical production is energy-intensive. In Europe, natural gas prices remain significantly higher than pre-crisis levels, rendering baseload production of commodities like ammonia and petrochemicals uncompetitive.

European Decline: European chemical production contracted in 2022 and 2023, and the recovery remains elusive. Major players continue to shut down crackers and rationalize assets. The “deindustrialization” of Europe is not a temporary phenomenon but a structural unwinding of capacity. Arkema (~€52, ~€4.0B market cap) reported FY2025 revenue down 5% to €9.07B with EBITDA of €1.25B at a 13.8% margin. The company is expanding PVDF capacity at Changshu, China (20% expansion, startup 2028) and Calvert City, KY (15% expansion, startup mid-2026) for battery and semiconductor markets, but 2026 guidance calls for only “slight EBITDA growth.” Solvay (~€24, ~€2.5B market cap), the post-demerger soda ash and peroxides business, delivered €881M EBITDA on €4.26B revenue but guides to lower 2026 EBITDA of €770–850M. At ~5.2–6.6× EV/EBITDA with a 12–14% FCF yield, Solvay screens as a deep value play. Morningstar’s fair value estimate of €74 is ~3× the current stock price.

US Dominance: US producers, leveraging Henry Hub natural gas pricing, are positioned to capture global market share. Companies like Westlake Corporation (WLK, ~$111, ~$14.3B market cap) and Olin Corporation (OLN, ~$26, ~$3.0B market cap) are prime beneficiaries. They operate in energy-intensive chains (chlor-alkali, PVC) where the US cost advantage translates directly into FCF margin expansion. Both companies are currently navigating a cyclical trough: Olin’s Q4 2025 adjusted EBITDA of $67.7M badly missed guidance, with full-year EBITDA landing at ~$585–635M, well below management’s mid-cycle bridge. Westlake booked $1.39B in identified items during 2025 reflecting the shutdown of three North American chlorovinyls plants, one styrene plant, and the Pernis (Netherlands) facility. However, Westlake’s three-pillar improvement plan targets $600M of incremental earnings in 2026 through structural cost cuts, closed-facility savings, and reliability improvements.

The AI “Cooling” Thesis: Fluoropolymers

While basic chemicals play a volume game, specialty chemicals are playing a technology game. The explosion of AI data centers has created a critical bottleneck: heat. High-performance GPUs (like Nvidia’s Blackwell architecture) generate immense thermal loads that traditional air cooling cannot manage. This is driving a transition to liquid cooling, specifically two-phase immersion cooling.

The fluids required for immersion cooling are often fluorinated chemistries (fluoropolymers) due to their dielectric properties and thermal stability. Furthermore, fluoropolymers are indispensable in the semiconductor manufacturing process itself, used in piping and storage for high-purity chemicals. The production of fluoropolymers is technically difficult and heavily regulated (PFAS regulations). This creates high barriers to entry.

Key Players:

The Chemours Company (CC, ~$17.81, ~$2.7B market cap): The AI cooling thesis is materializing. Chemours’ Thermal & Specialized Solutions segment delivered a record Q4 2025, with Opteon refrigerant sales growing 56% for the full year (now representing 75% of total refrigerant revenue, up from 56%). The company has signed a JDA with 2CRSi for Opteon two-phase immersion cooling, secured Samsung qualification for data center SSDs, and sizes the liquid cooling TAM at $550M by 2026, growing to $1.5B by 2030 and $3B by 2035. However, the balance sheet is stressed at ~$4.0B+ net debt with negative tangible book value, and PFAS liability remains the tail risk (the NJ settlement alone is $875M over 25 years). 2026 guidance calls for $800–900M adjusted EBITDA, implying ~9× EV/EBITDA at midpoint.

3M (MMM, ~$146, ~$76B market cap): The litigation overhang is clearing. The $6B earplug settlement has paid out over $3.1B with zero cases remaining. The $10.3B PFAS water contamination settlement received final court approval. FY2025 adjusted EPS came in at $8.06 (+10% YoY) with $4.4B in adjusted FCF. 2026 guidance of $8.50–$8.70 adjusted EPS implies continued mid-single-digit growth. The stock trades at ~17× forward P/E and ~11× EV/EBITDA with a 5.8% FCF yield.

Arkema & Solvay: European players expanding capacity (as detailed above), though they face structural energy headwinds. Arkema trades at ~5.2–6.1× EV/EBITDA with a 6.4–6.9% dividend yield.

Chlor-Alkali: The Building Block of Infrastructure

Chlor-alkali chemistry (producing chlorine and caustic soda) is the “bread and butter” of the industrial economy. Chlorine is essential for PVC (construction, pipes) and water treatment, while caustic soda is used in pulp & paper and aluminum refining.

The sector is characterized by a “co-product imbalance.” Demand for chlorine (construction-led) and caustic soda (industrial-led) rarely moves in sync, leading to volatile pricing. However, capacity rationalization in the US (Westlake shut three chlorovinyls plants in 2025) is restoring pricing power, and caustic soda inventories entered 2026 at very low levels.

The deployment of funds from the US Infrastructure Investment and Jobs Act (IIJA) serves as a long-term demand driver for PVC (pipes) and epoxy resins (coatings), directly benefiting the chlor-alkali chain. Westlake’s Housing, Infrastructure & Pipes (HIP) segment remains resilient, with 2026 guidance of $4.4–4.6B in HIP revenue at 19–21% EBITDA margins.

Olin Corporation (OLN) and Westlake Corporation (WLK) operate in an oligopolistic US market structure. With European capacity offline due to energy costs, these US producers effectively control the Atlantic basin marginal supply. Both are currently navigating a cyclical trough: Olin at ~9–10× TTM EV/EBITDA with 4.1× leverage and a Fitch downgrade to BB+, Westlake at ~15.5× TTM EV/EBITDA but with an investment-grade balance sheet (BBB+/BBB/Baa) and $2.9B in cash. The sector faces margin compression from Chinese capacity overexpansion and export “dumping,” but this is a cyclical rather than structural headwind. Olin has filed anti-dumping petitions on epoxy resins against five countries, and the EU imposed definitive duties on similar imports in July 2025.

Smart Money Endorsement

The sector’s strategic value was validated on January 2, 2026, when Berkshire Hathaway completed its $9.7 billion all-cash acquisition of OxyChem, Occidental Petroleum’s chemical division and a top-3 US manufacturer of PVC, chlor-alkali, and chlorinated organics. The deal valued OxyChem at ~8× projected 2025 EBITDA — Berkshire’s largest acquisition since the $11.6B Alleghany deal in 2022, consistent with Buffett’s preference for productive, cash-generating commodity assets bought at attractive cycle pricing. Occidental earmarked $6.5B of proceeds for debt reduction, and legacy environmental liabilities were retained by an Occidental subsidiary.

The gap between the Berkshire transaction multiple and current public trading multiples remains significant. Olin trades at ~9–10× TTM EV/EBITDA, but management’s mid-cycle EBITDA target of $2.0B (vs. ~$585–635M in 2025) implies a forward valuation of roughly 3.5×–4.0× on normalized earnings, supported by a $1.9B remaining share repurchase authorization (though buybacks have been curtailed to $50.5M in 2025 as management prioritizes deleveraging). Westlake trades at a higher optical multiple of ~15.5× TTM EV/EBITDA due to depressed earnings but is executing a $200M structural cost reduction program and targets $600M of incremental earnings in 2026.

Investors have the opportunity to acquire similar industrial infrastructure assets in the public markets at a discount to the price paid by a disciplined capital allocator, positioning themselves to benefit from the eventual recovery in global industrial demand. The entry point is cyclically depressed, which is precisely when Buffett chose to act.

Steel

Steel is often dismissed as a commoditized, cyclical industry. This view ignores the rapid technological stratification within the sector. The opportunity lies not in generic rebar, but in Grain-Oriented Electrical Steel (GOES) and high-strength alloys required for grid modernization and defense.

The Electrical Steel Bottleneck

There is no AI without electricity, and there is no electricity without transformers. Every step-up and step-down of voltage across the grid requires a transformer, and the core of every transformer is made of GOES.

The US suffers from a chronic shortage of distribution transformers, with lead times extending significantly. This shortage is exacerbated by the demand shocks from AI data centers, EV charging networks, and renewable energy interconnects. Producing GOES is technically demanding and capital intensive. There is limited domestic capacity in the US.

Cleveland-Cliffs (CLF, ~$8.03, ~$4.5B market cap) is the sole producer of GOES in North America, a natural monopoly on a critical national security asset. The company is in distressed territory today, with ~$7.2B net debt against essentially zero full-year EBITDA ($37M adjusted in FY2025), having burned $1.0B in FCF and issued 75M new shares. However, the turnaround thesis hinges on multiple catalysts converging in 2026–2027: the GOES expansion at Butler, PA (operational late 2026–early 2027); the Weirton, WV transformer plant (online H1 2026, ~$150M investment, adding 30–40% to GOES demand); 50% Section 232 tariffs on steel imports; a strategic MOU with POSCO for a ~$700M equity investment (≥10% stake, definitive agreement targeted H1 2026); and a $500M EBITDA improvement from terminating a slab supply contract.

Recent Department of Energy efficiency standards have confirmed the continued necessity of GOES (vs. amorphous metal alternatives), solidifying CLF’s market position. Section 232 tariffs now extend to downstream electrical steel laminations, preventing circumvention and protecting domestic margins. At 0.73× P/B and 0.21× P/S, CLF is deeply distressed but carries significant optionality.