We were delighted to welcome Christopher Tsai back to the Zurich Project, and we thank him for sharing his thinking so candidly with the group. Zurich Project proceedings are confidential by default; with Christopher’s approval, we are making the full session audio and transcript available below. The accompanying white paper, “Value Investing and the Emerging 4.0,” is available on the Tsai Capital website.

We are proud to feature a remarkable diversity of well-considered views under the Zurich Project / MOI Global / Latticework umbrella. One of the most gratifying realizations about The Zurich Project 2026 is that two market-beating investors and original thinkers, Chris Bloomstran and Christopher Tsai, came together in one room to present views that some will consider diametrically opposed. They did so respectfully and in a true spirit of learning and friendship. The same applies to the group as a whole. Over three days, we embarked on a genuine pursuit of truth, leaving ego at the door, asking questions, and seeking answers through open and honest debate.

A brief word on why this session is worth your time. Christopher is a third-generation investor and the son of Gerald Tsai Jr., who helped build Fidelity’s fund business, launched the Manhattan Fund in 1965, and became the first Chinese-American CEO of a DJIA company. Christopher founded Tsai Capital in 1997 and has compounded client capital ahead of the S&P 500 for more than two decades. He runs a concentrated portfolio shaped by Charlie Munger’s emphasis on quality, and his largest and most debated position, Tesla, bought in early 2020, runs through much of the conversation. For more of his thinking, revisit his Latticework 2025 keynote fireside chat.

What follows is our executive summary of Christopher Tsai’s session; the full detail and the complete Q&A sit in the materials below.

One discipline, four eras

Christopher’s organizing idea is that value investing has passed through three distinct eras and is entering a fourth, with each step extending the time horizon over which value is created and lowering the odds of success. He borrows David Foster Wallace’s “This is Water” parable: the most important realities are the hardest to see because they surround us.

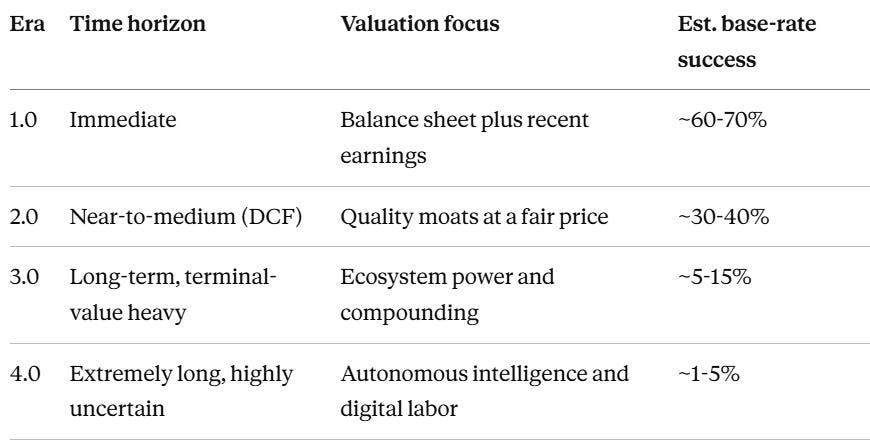

Value Investing 1.0, born in the Great Depression, meant buying assets below liquidation value. Graham’s net-nets, laid out in the 1934 edition of Security Analysis, let you buy a company for less than two-thirds of its net current assets and get the plant and equipment for free. Value was immediate and sat on the balance sheet. By Christopher’s estimate, roughly 60% to 70% of disciplined 1.0 practitioners earned durable returns, the highest hit rate of any era, because the value was already there to be unlocked.

Value Investing 2.0 is the Buffett and Munger shift from “cheap” to “a wonderful business at a fair price.” The Coca-Cola purchase announced it to the world. Moats, brands, and early network effects replaced hard assets as the source of value, and discounted future cash flows replaced the balance sheet as the unit of analysis. Estimated success rate: 30% to 40%.

Value Investing 3.0 adapts to platforms that deliberately suppress current profit to fund reinvestment. Drawing on Marshall McLuhan, Christopher reframes “the medium is the message” as “the medium is the moat”: the best companies architect ecosystems that change how we live and transact, with Apple’s 2007 iPhone the clearest early case. Power laws rule, Metcalfe’s Law compounds network value, and outcomes are radically unequal. Success rate: 5% to 15%.

The 3.0 mechanics worth stealing

Two ideas from the 3.0 section deserve emphasis. First, Christopher builds on Nick Sleep’s “scale economies shared” by splitting it in two. The supply side is familiar: Amazon, Tesla, and Starlink push falling unit costs back to customers as lower prices, feeding a flywheel. The demand side is his own contribution. When a product is already free, like Google Search or Instagram, the company cannot cut price, so it compounds value through what he calls “Engagement Value per Unit Time”: lower latency, better reliability, richer personalization. It is harder to see, “like water to a fish,” but no less powerful.

Second, latent pricing power. Christopher prizes businesses that could raise prices but choose not to, because restraint extends the runway and builds customer goodwill. The tell shows up in gross margins held high through inflation or supply shocks. He contrasts this with TransDigm and HEICO, fine businesses that raise prices continuously, which is precisely what he is not looking for. The practical payoff: a company can look expensive on reported earnings and be cheap on intrinsic value.

His archetype is Tesla. When Tsai Capital bought in 2020, the price worked out to roughly 65 times earnings, closer to 25 times normalized, and about 3 times revenue, with the embedded businesses (autonomy, robotics) essentially free. He concedes some of his projections were well off. The position still returned roughly 11 times in six years, and he believes the compounding is early. He also places MSCI, Moody’s, S&P, and Broadridge in the 3.0 camp.

The 4.0 test

Value Investing 4.0 is where Christopher is now pointing. The economic castle is no longer a brand or an ecosystem but intelligence itself. Using graph theory, he calls intelligence the “edge” on which operating businesses, the “nodes,” are built. In a 3.0 business the edge already exists and the nodes are profitable; in a 4.0 business the edge still has to be built, so the nodes are in their infancy, if they exist at all. He defines a true 4.0 business by four tests:

Intelligence itself as the economic castle (the edge)

Digital labor as the core output customers buy

A self-sustaining model

The capacity to deploy enormous capital at high rates of return over a long duration

His blunt conclusion: no independent, publicly traded 4.0 business exists today [ed. note: this may have changed with the SpaceX IPO]. They are all incubated inside larger 3.0 parents, with Tesla (Dojo, FSD, Optimus) the most advanced public example and the frontier labs (Anthropic, OpenAI, xAI) the heavily funded private ones. The base rate here is brutal, on his numbers 1% to 5%.

The economics he is watching

This is where the talk gets concrete. Christopher walked through the xAI and Anthropic compute relationship as a live example of 4.0 economics. xAI built two data centers, Colossus 1 at roughly $7 billion and Colossus 2 at an estimated $23 billion, about $30 billion combined. Per Anthropic’s S-1, Anthropic is buying compute from xAI at an equivalent of about $15 billion per year. At roughly 50% gross margins, that is about $7.5 billion of gross profit a year, and the facility is running at only about 15% of capacity. Over a four-year contract, that implies roughly $60 billion of revenue and about a 100% return on the $30 billion of capital.

He addressed the bear signal directly. Elon Musk later noted a 90-day termination clause rather than a fixed four-year term, and the market sold off before recovering. Christopher reads the tweet as a sign of strength, not weakness, since Anthropic is severely compute-constrained and may receive less capacity, not more, which would raise xAI’s return. He cited Jensen Huang’s view that Anthropic could grow from a roughly $30 billion revenue run rate to $1 trillion within five years; if anything close to that holds, compute demand dwarfs $15 billion a year. He was careful to say the economics are powerful but their durability is unproven. He also flagged Berkshire’s reported participation in an ~$80 billion Google raise, about 2% of its market cap, earmarked for AI, as another 4.0 effort funded through a 3.0 parent.

Valuing the unknowable

How do you underwrite this? Christopher uses historical base rates as priors, then updates them Bayesian-style as evidence arrives, thinking in terms of return “vectors” rather than point estimates. Because uncertainty rises with each era, the margin of safety must rise too. His central move is the one Tesla taught him: buy the 4.0 optionality embedded inside a 3.0 business at as close to zero incremental cost as possible. Selectivity, he stressed, matters more here than anywhere else on the spectrum. On portfolio construction, he makes the case for “planting more seeds,” owning more names than a typical concentrated manager, while refusing to “cut flowers to water weeds.”

From the Q&A

The audience pushed hard, and the exchanges are some of the best material. One member argued the large language models themselves are commodities, noting China has over a thousand registered models and drawing the early-auto-industry analogy. Christopher largely agreed: base rates are low, most will not survive, and the winners will compete on infrastructure, data, and energy cost per token. But a commodity is fine if you are the low-cost producer, as Nucor has shown in steel. He also detailed his scoring system, 48 points across four pillars (capital allocation, secular tailwinds, operational excellence, and moat), which feeds position sizing alongside expected IRR. He closed on Peter Kaufman’s “one ladder” model for a life well lived.

Listen to the full session

The summary above is only the outline. The audio replay and transcript carry the full argument, the supporting data, and the Q&A, including his test for telling a genuinely differentiated intelligence architecture from a well-funded experiment. Set aside the time and listen closely. It is some of the clearest thinking we have heard on where value investing goes next.