In a recent post, we looked at ways to invest in the AI data storage boom without paying up. Today, we examine critically the data storage darlings themselves. We do so not because Western Digital, Seagate, and SanDisk are bad companies, but because they have been swept up in a mania that rhymes with the turn-of-the-century tech stock mania. Investors tend to have short memories, and this is a case in point.

It’s clear why this piece may be relevant to long/short investors, but why should long-only investors care? The answer is simple: When the unraveling comes, it may affect a broader swath of equities than many of us may like to admit. Companies such as Alphabet, Microsoft, TSMC, and numerous others that may appear reasonably valued at the moment will not be immune to the negativity that comes with post-bubble disillusionment.

This piece lays out a path for how the bubble may unravel. While focused on the high-flying data storage darlings, the potential sequence of events is instructive to investors in adjacent tech segments as well.

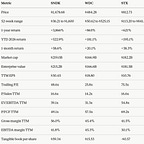

Table: The Current Mania, Quantified

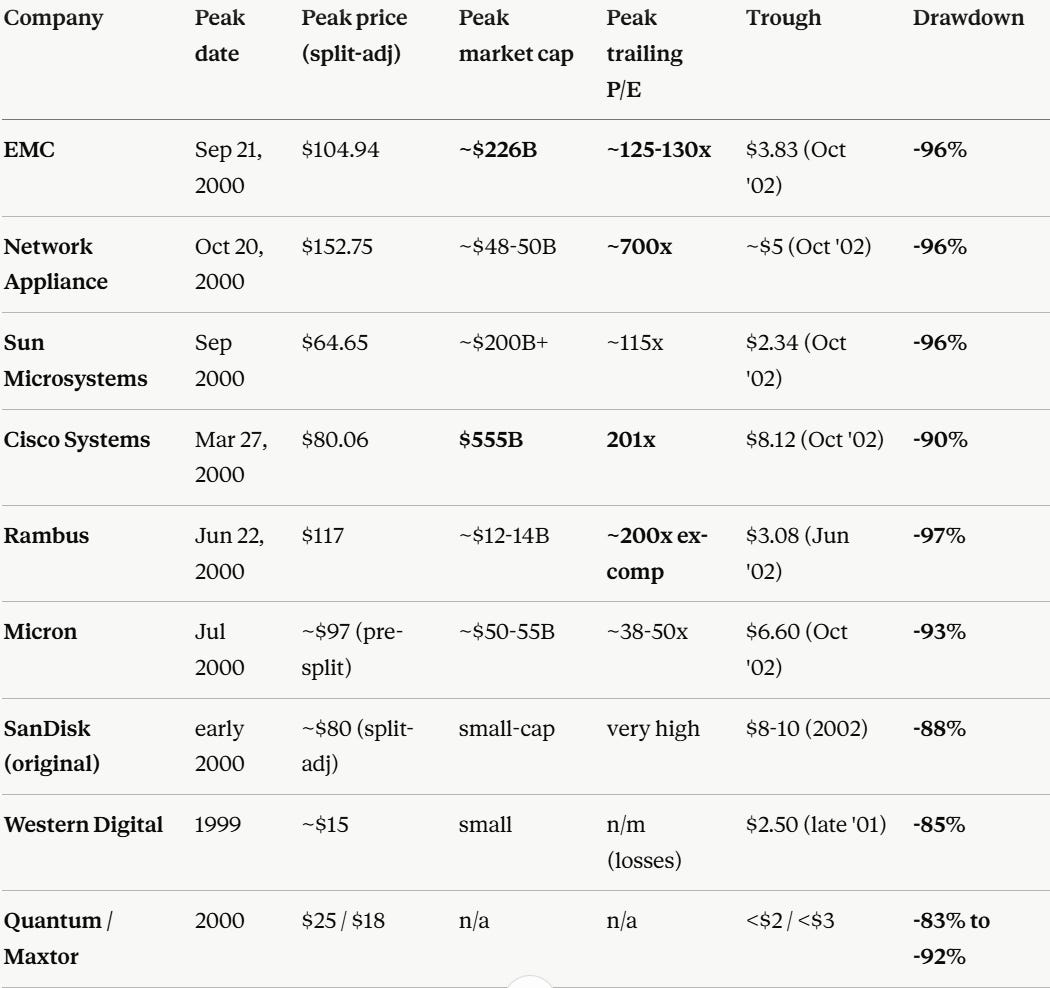

The storage and memory complex is exhibiting mania characteristics that exceed the equivalent storage/memory cohort of 1999-2000 on most measurable axes. SanDisk (SNDK) trades at $1,478, up 3,866% over one year and 523% year-to-date. Western Digital (WDC) trades at $484, up 865% over one year and 181% YTD. Seagate (STX) trades at $812, up 621% over one year and 195% YTD. The trio carries a combined market cap of $568 billion. The peak-valuation comparables of the prior cycle, including EMC at 125-130x P/E, NetApp at ~700x P/E, Rambus at ~200x P/E, and Cisco at 201x P/E, eventually drew down 90 to 97 percent over the following 24 to 30 months.

Today’s stocks trade at trailing P/Es of 26 to 76x and 14 to 17x trailing sales on share prices that have advanced 9 to 40 times in 12 to 15 months. The mechanical analogue is uncomfortably tight; the differences are real but narrower than the bull narrative suggests.

Table: Peak Valuations and Drawdowns, Prior Cycle

This article quantifies the current setup, anchors it to the 1999-2000 mania with hard valuation numbers, builds a structured catalyst framework for the bear case, and sketches an unravel scenario. The bull case has genuine merit: hyperscaler capex visibility ($725 billion committed for 2026 by the Big Four alone, up 77% year-over-year), oligopolistic industry structure (HDD is now a three-player market), supply discipline in NAND, and real prepaid multi-year long-term agreements (LTAs) from creditworthy customers. But at current valuations the margin of safety is negative on any normalized earnings framework, and several of the leading indicators of cycle peak are already flickering.